This report was recently updated on April 14 2025 with the latest and most recent

market numbers

Global Medical Device Connectivity Market Size, Trends, and Analysis - Forecasts To 2026 By Product & Service (Medical Device Connectivity Solutions (Medical Device Integration, Interface Devices, Connectivity Hubs, Telemetry Systems), Medical Device Connectivity Services (Support and Maintenance, Implementation and Integration, Training, Consulting)), By Technology (Wired Technologies, Wireless Technologies, Hybrid Technologies), By End-User (Hospitals,Home Healthcare Centers, Diagnostic and Imaging Centers, Ambulatory Care Centers), By Region (North America, Asia Pacific, CSA, Europe, and the Middle East and Africa); End-User Landscape, Company Market Share Analysis & Competitor Analysis

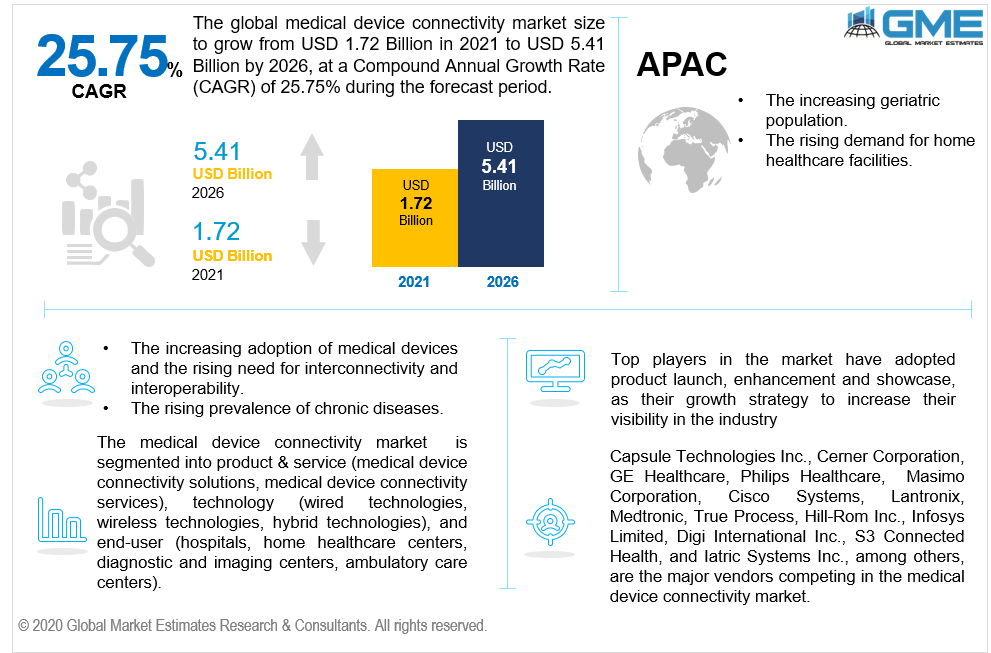

Technological advancements in the fields of information technology & communications and medical devices have resulted in the growing demand for increased interconnectivity and interoperability between medical devices. Smart medical devices that can record and present information to the users are becoming increasingly common in healthcare institutes and have resulted in the growth of the global medical device connectivity market. The interconnected devices are capable of improving the efficiency of caregivers as it lessens nursing hours spent on patients as they can be monitored remotely and caregivers are alerted to changes through the devices. The growing demand and need for data analytics among healthcare facilities and the growing adoption of analytical technologies to analyze patient data & EHR's in healthcare organizations and hospitals are supporting the market growth. The market is restrained by the high cost of implementation, data privacy and safety concerns, and the reluctance of healthcare workers to implement such devices.

The global market can be segmented into medical device connectivity solutions and services based on product & services. The segment includes medical device integration, telemetry systems, interface devices, and connectivity hubs among others. The solutions segment holds the maximum share of the market with the medical device integration subsegment growing at the fastest rate. The growing need to implement medical device connectivity through the integration of existing devices and newer devices is the major driving force of this segment.

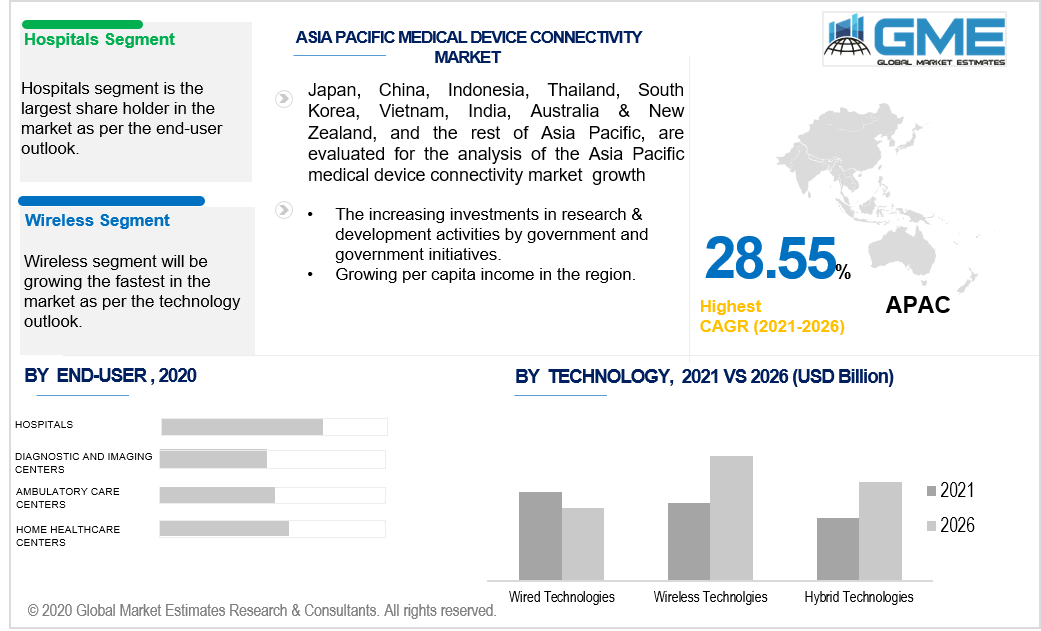

Hybrid technologies, wired technologies, and wireless are the major technologies used in medical device connectivity. The wireless segment was the dominant segment in the market. The ease of using wireless technologies combined with their extended-range and ability to provide real-time updates has made them the dominant segment compared to wired and hybrid technologies. Wireless technologies help physicians and caretakers to monitor patients 24/7 and help to offer faster treatment servicesto required patients. The easy handling of wireless devices is also promoting the market growth between the forecast period.

Based on the end-user analysis, the hospital segment held the dominant share of the market and expected to continue the trend between the forecast period. The rising number of hospitals and their ability to bear the high implementation cost of interconnected medical devices have resulted in them dominating the market. Hospitals have the added benefit of favorable healthcare policies and insurance coverage to cover the costs of implementing such devices. According to research, there are approximately 6090 reputed hospitals in the U.S., in which 208 hospitals are federal government hospitals and 625 are nonfederalpsychiatric hospitals.

The North American region was the dominant market owing to the larger expenditure on healthcare due to the large percentage of the geriatric population in this region. The presence of developed nations including the U.S. and Canada is also boosting regional growth. The U.S. is one of the prominent countries in the world that allocates huge investments in new technologies. The increased penetration and adoption of technological advancements in this region are also major drivers of the market in this region. The increased automation in healthcare devices and growing demand for health services are positively impacting the market growth. The APAC region registers a tremendousgrowth market among all regions. The increasing expenditure on healthcare due to the rise in incidences of chronic diseases and the increasing geriatric population have contributed to the growth in this region. The region has also seen an increase in the number of medical device connectivity vendors which has helped reduce the cost of such systems. The growing per capita income in the region, increasingly positive government initiatives, and increased expenditure on R&D are all expected to have a positive influence on the growth of the market in this region.

Cerner Corporation, Capsule Technologies Inc, GE Healthcare, Philips Healthcare, Masimo Corporation, Cisco Systems, Lantronix, Medtronic, True Process, Hill-Rom Inc., Infosys Limited, iHealth Labs, Bridge-Tech Medical Inc., MediCollector LLC, Spectrum Medical Ltd., Silex Technology Inc., TE Connectivity, Digi International Inc., S3 Connected Health, and Iatric Systems Inc.,among others,are the key players involved in the development of advanced medical technologies.

Please note: This is not an exhaustive list of companies profiled in the report.

In January 2021, Capsule Technologies was sold to Philips for USD 635 million by Fransico Partners. The company had recently announced its collaboration with Retia MEidcla to integrate Capsule’s Device Driver Integration (DDI) to Retia’s Argos cardiac monitor range.

In January 2021, Cerner Corporation began to provide their Electron Health Record services to 12 behavioral health facilities across the state of Virginia, USA.

Masimo Corporation signed a contractin June 2020, to purchase NantHealth’s connected care business.

We value your investment and offer free customization with every report to fulfil your exact research needs.

The Global Medical Device Connectivity Market has been studied from the year 2019 till 2026. However, the CAGR provided in the report is from the year 2021 to 2026. The research methodology involved three stages: Desk research, Primary research, and Analysis & Output from the entire research process.

The desk research involved a robust background study which meant referring to paid and unpaid databases to understand the market dynamics; mapping contracts from press releases; identifying the key players in the market, studying their product portfolio, competition level, annual reports/SEC filings & investor presentations; and learning the demand and supply-side analysis for the Medical Device Connectivity Market.

The primary research activity included telephonic conversations with more than 50 tier 1 industry consultants, distributors, and end-use product manufacturers.

Finally, based on the above thorough research process, an in-depth analysis was carried out considering the following aspects: market attractiveness, current & future market trends, market share analysis, SWOT analysis of the company and customer analytics.

This FREE sample includes market data points, ranging from trend analyses to market estimates & forecasts. See for yourself.

Or view our licence options:

Tailor made solutions just for you

80% of our clients seek made-to-order reports. How do you want us to tailor yours?

OUR CLIENTS