This report was recently updated on April 22 2025 with the latest and most recent

market numbers

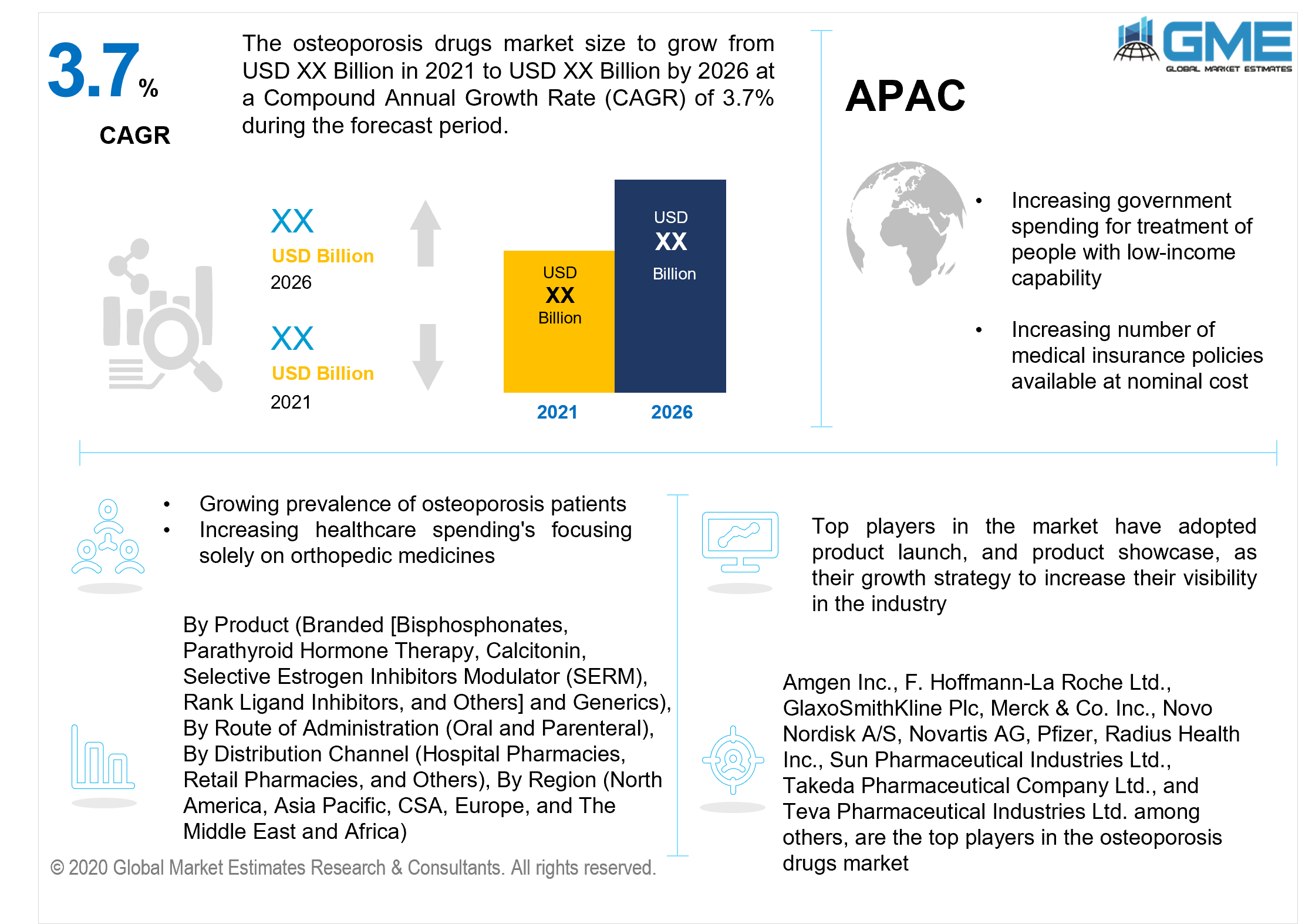

Global Osteoporosis Drugs Market Size, Trends & Analysis - Forecasts to 2026 By Product (Branded [Bisphosphonates, Parathyroid Hormone Therapy, Calcitonin, Selective Estrogen Inhibitors Modulator (SERM), Rank Ligand Inhibitors, and Others] and Generics), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), By Region (North America, Asia Pacific, CSA, Europe, and The Middle East and Africa); Competitive Landscape, Company Market Share Analysis, and Competitor Analysis

Osteoporosis is a pathological disease that is characterized by reduced bone density and consistency in humans. Moreover, in this medical state, the bones turn brittle, making them more flexible and vulnerable to fractures. The disease is triggered by an excess production of the parathyroid hormone. The disease can result in serious fractures, which can be harmful to the person's condition. As a result, the disease necessitates surgery, which involves the incorporation of osteoporosis medications.

The rising prevalence of osteoporosis is a significant factor contributing to the market's expansion. As per the National Osteoporosis Foundation, approximately 10 million individuals in the United States reported osteoporosis in 2018, with another 44 million having reduced bone mass, putting them at elevated risk. Another major factor driving demand growth is the world's growing elderly demographic, which is vulnerable to low bone density. According to statistics released by the International Osteoporosis Foundation in 2020, 1 in 5 men and 1 in 3 women over the age of 50 may suffer osteoporosis injuries in their subsequent lifespans worldwide.

Moreover, increasing expenditures on R&D by biotechnology and pharmaceutical firms are driving business growth. For example, in October 2020, the Italian pharmaceutical federal agency approved human clinical studies for raloxifene, a standard osteoporosis medication that scientists hope will also help alleviate COVID-19 complications and render patients least infectious. Thus, optimistic clinical trial outcomes could contribute to novel medication alternatives, fueling market growth in the future. Government controls, on the other hand, are significant impediments to business development.

The possible factors acting as restraints for the market are the severe side effects that the medicines used for the treatment have on the body. Also, medications for treatment have limited reach globally, reducing the exposure of the drugs and treatment for osteoporosis among people.

Furthermore, the volume of patent expirations is increasing therapeutic pressure to using generic forms of existing drugs, which is expected to intensify the generic osteoporosis drugs market throughout the forecast period. The foregoing reasons, taken together, are expected to provide them with significant potential growth prospects in the near future. Moreover, an expansion in the volume of programs to raise consciousness rates about osteoporosis treatment amongst patients and doctors is projected to broaden the osteoporosis market development prospects throughout the forecast period.

Based on product, osteoporosis drugs can be segregated as branded and generics. Branded medicines are further classified as bisphosphonates, parathyroid hormone therapy, calcitonin, selective estrogen inhibitors modulator (SERM), rank ligand inhibitors, and others. Branded medicines are likely to be the highest-selling product as a result of increased spending by key players in the research and development activities of innovative novel drugs. Moreover, these drugs are often used as medications for the treatment of osteoporosis, which drives demand development. They have been proved to be extremely efficient for the treatment of women between the age of 60 and 90 years suffering from osteoporosis as it has been proved to be highly efficient in increasing the metabolism of the bone.

Depending on the administration route, market can be segregated as oral and parenteral. The parenteral route of administration is presumed to lead the market due to increased use of parenteral products, which account for 70% of the sales in the osteoporosis drug market. Along with, due to higher bioavailability and a faster mechanism of action, there is expanded use of the parenteral drug which is resulting in increased global demand. This is presumed to have a significant effect on the segment's development throughout the forecast period.

Depending on the distribution channel, market can be segregated as hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacy is likely to lead in this segment. A surge in the proportion of patients attending hospitals for osteoporosis care, effective government funding for hospital pharmacy expansion, and other variables are propelling the growth of hospital pharmacies.

The osteoporosis drugs market by region can be classified into North America (the US, Canada, and Mexico), Asia Pacific (India, China, Japan, Malaysia, Singapore, and Rest of Asia Pacific), Europe (Germany, United Kingdom, Italy, France, Spain, Netherlands, and Rest of Europe), Middle East & Africa and Central & South America. North America is dominating the market due to the high number of osteoporosis patients in Canada and United States of America, which has been rising every year. The government has also been organizing awareness programs for people to decrease osteoporosis cases in the region, such as malnutrition programs for unprivileged children, encouraging people by organizing fitness campaigns, organizing medical campaigns for people to inform them about the good effects of a perfectly balanced diet that is full of proteins and calcium which can help prevent osteoporosis. Owing to its high-class healthcare system, the orthopedic department in the hospitals is equipped with high-tech types of equipment for surgical procedures and an increasing number of dedicated orthopedic clinics and hospitals for the treatment of osteoporosis. The Asia Pacific is the leader in regard to CAGR, owing to its rapid development in healthcare services and increased government spending for the treatment of people with low-income capability. Also, the increasing research in the Indian, Chinese and Japanese medical fields for the treatment of bone-related diseases has been driving the Asia Pacific market. Also, the increasing volume of medical insurance policies available at a nominal cost that could be affordable by any person with mid-income is increasing the proportion of treatments in the region. Infrastructural development in hospitals for orthopedic surgeries and treatment has been on the rise in the Indian subcontinent, thus, leading to the robust growth in the osteoporosis drug market of APAC.

Amgen Inc., F. Hoffmann-La Roche Ltd., GlaxoSmithKline Plc, Merck & Co. Inc., Novo Nordisk A/S, Novartis AG, Pfizer, Radius Health Inc., Sun Pharmaceutical Industries Ltd., Takeda Pharmaceutical Company Ltd., and Teva Pharmaceutical Industries Ltd. among others, are the top players in the osteoporosis drugs market.

Please note: This is not an exhaustive list of companies profiled in the report.

Chapter 1 Methodology

1.1 Market Scope & Definitions

1.2 Estimates & Forecast Calculation

1.3 Historical Data Overview And Validation

1.4 Data Products

1.4.1 Secondary

1.4.2 Primary

Chapter 2 Report Outlook

2.1 Osteoporosis Drugs Market Overview, 2016-2026

2.1.1 Industry Overview

2.1.2 Product Overview

2.1.3 Route of Administration Overview

2.1.4 Distribution Channel Industry Overview

2.1.5 Regional Overview

Chapter 3 Osteoporosis Drugs Market Trends

3.1 Market Segmentation

3.2 Industry Background, 2016-2026

3.3 Market Key Trends

3.3.1 Positive Trends

3.3.1.1 Surge in Geriatric Population

3.3.1.2 Rise in Adoption of Sedentary Lifestyle

3.3.2 Industry Challenges

3.3.2.1 Time-Consuming Drug Approval Process

3.4 Prospective Growth Scenario

3.4.1 Product Growth Scenario

3.4.2 Route of Administration Growth Scenario

3.4.3 Distribution Channel Growth Scenario

3.5 COVID-19 Influence over Industry Growth

3.6 Porter’s Analysis

3.7 PESTEL Analysis

3.8 Value Chain & Supply Chain Analysis

3.9 Regulatory Framework

3.9.1 North America

3.9.2 Europe

3.9.3 APAC

3.9.4 LATAM

3.9.5 MEA

3.10 Technology Overview

3.11 Market Share Analysis, 2020

3.11.1 Company Positioning Overview, 2020

Chapter 4 Osteoporosis Drugs Market, By Product

4.1 Product Outlook

4.2 Branded

4.2.1 Market Size, By Region, 2016-2026 (USD Million)

4.3 Bisphosphonates

4.3.1 Market Size, By Region, 2016-2026 (USD Million)

4.4 Parathyroid

4.4.1 Market Size, By Region, 2016-2026 (USD Million)

4.5 Hormone Therapy

4.5.1 Market Size, By Region, 2016-2026 (USD Million)

4.6 Calcitonin

4.6.1 Market Size, By Region, 2016-2026 (USD Million)

4.7 Selective Estrogen Inhibitors Modulator (SERM)

4.7.1 Market Size, By Region, 2016-2026 (USD Million)

4.8 Rank Ligand Inhibitors

4.8.1 Market Size, By Region, 2016-2026 (USD Million)

4.9 Others

4.9.1 Market Size, By Region, 2016-2026 (USD Million)

4.10 Generics

4.10.1 Market Size, By Region, 2016-2026 (USD Million)

Chapter 5 Osteoporosis Drugs Market, By Route of Administration

5.1 Route of Administration Outlook

5.2 Oral

5.2.1 Market Size, By Region, 2016-2026 (USD Million)

5.3 Parenteral

5.3.1 Market Size, By Region, 2016-2026 (USD Million)

Chapter 6 Osteoporosis Drugs Market, By Distribution Channel Industry

6.1 Distribution Channel Industry Outlook

6.2 Hospital Pharmacies

6.2.1 Market Size, By Region, 2016-2026 (USD Million)

6.3 Retail Pharmacies

6.3.1 Market Size, By Region, 2016-2026 (USD Million)

6.4 Others

6.4.1 Market Size, By Region, 2016-2026 (USD Million)

Chapter 7 Osteoporosis Drugs Market, By Region

7.1 Regional outlook

7.2 North America

7.2.1 Market Size, By Country 2016-2026 (USD Million)

7.2.2 Market Size, By Product, 2016-2026 (USD Million)

7.2.3 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.2.4 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.2.5 U.S.

7.2.5.1 Market Size, By Product, 2016-2026 (USD Million)

7.2.5.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.2.5.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.2.6 Canada

7.2.6.1 Market Size, By Product, 2016-2026 (USD Million)

7.2.6.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.2.6.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3 Europe

7.3.1 Market Size, By Country 2016-2026 (USD Million)

7.3.2 Market Size, By Product, 2016-2026 (USD Million)

7.3.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.4 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.5 Germany

7.3.5.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.5.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.5.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.6 UK

7.3.6.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.6.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.6.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.7 France

7.3.7.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.7.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.7.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.8 Italy

7.3.8.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.8.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.8.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.9 Spain

7.3.9.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.9.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.9.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.3.10 Russia

7.3.10.1 Market Size, By Product, 2016-2026 (USD Million)

7.3.10.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.3.10.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4 Asia Pacific

7.4.1 Market Size, By Country 2016-2026 (USD Million)

7.4.2 Market Size, By Product, 2016-2026 (USD Million)

7.4.3 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.4.4 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4.5 China

7.4.5.1 Market Size, By Product, 2016-2026 (USD Million)

7.4.5.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.4.5.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4.6 India

7.4.6.1 Market Size, By Product, 2016-2026 (USD Million)

7.4.6.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.4.6.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4.7 Japan

7.4.7.1 Market Size, By Product, 2016-2026 (USD Million)

7.4.7.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.4.7.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4.8 Australia

7.4.8.1 Market Size, By Product, 2016-2026 (USD Million)

7.4.8.2 Market size, By Route of Administration, 2016-2026 (USD Million)

7.4.8.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.4.9 South Korea

7.4.9.1 Market Size, By Product, 2016-2026 (USD Million)

7.4.9.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.4.9.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.5 Latin America

7.5.1 Market Size, By Country 2016-2026 (USD Million)

7.5.2 Market Size, By Product, 2016-2026 (USD Million)

7.5.3 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.5.4 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.5.5 Brazil

7.5.5.1 Market Size, By Product, 2016-2026 (USD Million)

7.5.5.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.5.5.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.5.6 Mexico

7.5.6.1 Market Size, By Product, 2016-2026 (USD Million)

7.5.6.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.5.6.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.5.7 Argentina

7.5.7.1 Market Size, By Product, 2016-2026 (USD Million)

7.5.7.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.5.7.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.6 MEA

7.6.1 Market Size, By Country 2016-2026 (USD Million)

7.6.2 Market Size, By Product, 2016-2026 (USD Million)

7.6.3 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.6.4 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.6.5 Saudi Arabia

7.6.5.1 Market Size, By Product, 2016-2026 (USD Million)

7.6.5.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.6.5.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.6.6 UAE

7.6.6.1 Market Size, By Product, 2016-2026 (USD Million)

7.6.6.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.6.6.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

7.6.7 South Africa

7.6.7.1 Market Size, By Product, 2016-2026 (USD Million)

7.6.7.2 Market Size, By Route of Administration, 2016-2026 (USD Million)

7.6.7.3 Market Size, By Distribution Channel Industry, 2016-2026 (USD Million)

Chapter 8 Company Landscape

8.1 Competitive Analysis, 2020

8.2 Amgen Inc.

8.2.1 Company Overview

8.2.2 Financial Analysis

8.2.3 Strategic Positioning

8.2.4 Info Graphic Analysis

8.3 F. Hoffmann-La Roche Ltd.

8.3.1 Company Overview

8.3.2 Financial Analysis

8.3.3 Strategic Positioning

8.3.4 Info Graphic Analysis

8.4 GlaxoSmithKline Plc

8.4.1 Company Overview

8.4.2 Financial Analysis

8.4.3 Strategic Positioning

8.4.4 Info Graphic Analysis

8.5 Merck & Co. Inc.

8.5.1 Company Overview

8.5.2 Financial Analysis

8.5.3 Strategic Positioning

8.5.4 Info Graphic Analysis

8.6 Novo Nordisk A/S

8.6.1 Company Overview

8.6.2 Financial Analysis

8.6.3 Strategic Positioning

8.6.4 Info Graphic Analysis

8.7 Novartis AG, UEZ

8.7.1 Company Overview

8.7.2 Financial Analysis

8.7.3 Strategic Positioning

8.7.4 Info Graphic Analysis

8.8 Pfizer

8.8.1 Company Overview

8.8.2 Financial Analysis

8.8.3 Strategic Positioning

8.8.4 Info Graphic Analysis

8.9 Radius Health Inc.

8.9.1 Company Overview

8.9.2 Financial Analysis

8.9.3 Strategic Positioning

8.9.4 Info Graphic Analysis

8.10 Sun Pharmaceutical Industries Ltd.

8.10.1 Company Overview

8.10.2 Financial Analysis

8.10.3 Strategic Positioning

8.10.4 Info Graphic Analysis

8.11 Takeda Pharmaceutical Company Ltd.

8.11.1 Company Overview

8.11.2 Financial Analysis

8.11.3 Strategic Positioning

8.11.4 Info Graphic Analysis

8.12 Teva Pharmaceutical Industries Ltd.

8.12.1 Company Overview

8.12.2 Financial Analysis

8.12.3 Strategic Positioning

8.12.4 Info Graphic Analysis

8.13 Other Companies

8.13.1 Company Overview

8.13.2 Financial Analysis

8.13.3 Strategic Positioning

8.13.4 Info Graphic Analysis

The Global Osteoporosis Drugs Market has been studied from the year 2019 till 2026. However, the CAGR provided in the report is from the year 2021 to 2026. The research methodology involved three stages: Desk research, Primary research, and Analysis & Output from the entire research process.

The desk research involved a robust background study which meant referring to paid and unpaid databases to understand the market dynamics; mapping contracts from press releases; identifying the key players in the market, studying their product portfolio, competition level, annual reports/SEC filings & investor presentations; and learning the demand and supply-side analysis for the Osteoporosis Drugs Market.

The primary research activity included telephonic conversations with more than 50 tier 1 industry consultants, distributors, and end-use product manufacturers.

Finally, based on the above thorough research process, an in-depth analysis was carried out considering the following aspects: market attractiveness, current & future market trends, market share analysis, SWOT analysis of the company and customer analytics.

Frequently Asked Questions

![Global Osteoporosis Drugs Market Size, Trends & Analysis - Forecasts to 2026 By Product (Branded [Bisphosphonates, Parathyroid Hormone Therapy, Calcitonin, Selective Estrogen Inhibitors Modulator (SERM), Rank Ligand Inhibitors, and Others] and Generics), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), By Region (North America, Asia Pacific, CSA, Europe, and The Middle East and Africa); Competitive Landscape, Company Market Share Analysis, and Competitor Analysis](https://www.globalmarketestimates.com/images/cat/Healthcare.png)

This FREE sample includes market data points, ranging from trend analyses to market estimates & forecasts. See for yourself.

Or view our licence options:

Tailor made solutions just for you

80% of our clients seek made-to-order reports. How do you want us to tailor yours?

OUR CLIENTS